Everything has its own particular confinements, so is the CVP. Indeed, even CVP is valuable and critical instrument for directors, it have a few its own constraints. While applying CVP examination, inferring conclusions, chief ought to take a gander at its premises to settle on choice unprejudiced and clear. CVP investigation depends on a few presumptions which limited it with in a region restricting its frame of reference. A few suppositions or restrictions of CVP are said beneath.

1. CVP investigation is done just under variable costing wage explanation position it organization is utilizing another configuration then it is difficult to discover relationship.

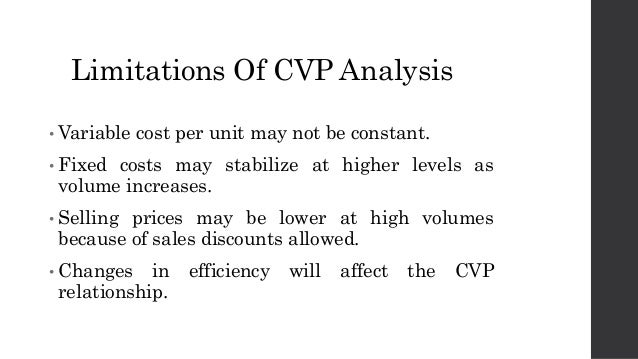

2. CVP investigation requires isolation of expense to settled and variable. By and by, the cost isolation is troublesome assignment and its exactness is in uncertainty. In this way, conclusions get from it make get to be fake.

3. CVP accept that offering value, costs stay straight in future whatever yield is produce. As a general rule, due to rivalry and different components causes vacillation on costs, offering cost and deals unit.

4. It further expect that profitability and effectiveness of representatives and machines are not going to change all through important scope of generation. It disregards the financial law of scale.

5. It do take thought of present estimation of cash (Money got today is more profitable than it get in tomorrow.).

6. Then again, it depends on the unrealistic methodology that economic situation and item blend would stay same in future.

What number of constraints it might have, yet at the same time it is valuable and imperative instrument of administrative bookkeeping. It helps administrators to discovering the most ideal blends of variable costs, altered cost, offering value, deals volume and blend of items to offer. It furnishes the chiefs with an effective apparatus for distinguishing those blueprints that will and won't enhance benefit.

No comments:

Post a Comment